We use necessary cookies to make our site work. We'd also like to set analytics cookies that help us make improvements by measuring how you use the site. These will be set only if you accept. For more detailed information about the cookies we use, see our Privacy Notice for more information.

Unsecured lenders need a fast, reliable way to verify an applicant’s income. Experian Verify brings Open Banking, payroll, HMRC data and supporting documents into one seamless applicant journey.

WRITTEN BY

Chris Milligan

PUblished ON

May 18, 2026

For unsecured lenders, income verification needs to happen as quickly and easily as possible. Applicants expect a fast digital journey, while lenders need confidence in an applicant’s income to assess affordability effectively. In practice, the challenge is rarely a lender’s own affordability policies. It is the way income evidence is verified and moved through the application journey.

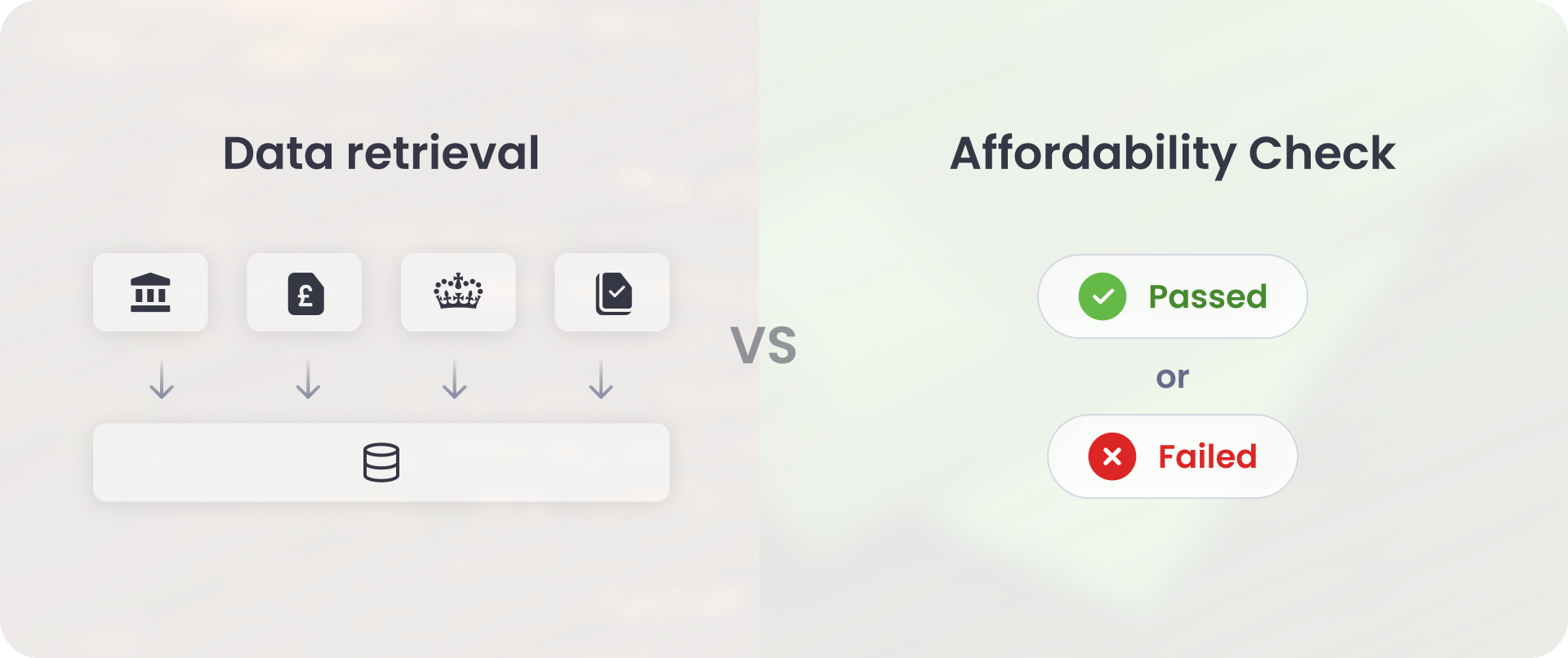

Current Account Turnover (CATO) data, such as that delivered through Experian’s Affordability IQ product, can provide a valuable way to sense check applicant-declared income and support affordability calculations. But in many cases, lenders still need additional evidence to confirm income more fully. That can mean drawing on sources such as Open Banking, payroll data, HMRC records, or supporting documents before an applicant’s income can be verified with confidence. In unsecured lending, that often creates resource-heavy manual processes and a potentially slower applicant experience.

This becomes more important when affordability calculations sit inside a wider lending workflow. When income verification is fragmented, the process around the calculation becomes slower and harder to manage operationally, technically, and commercially.

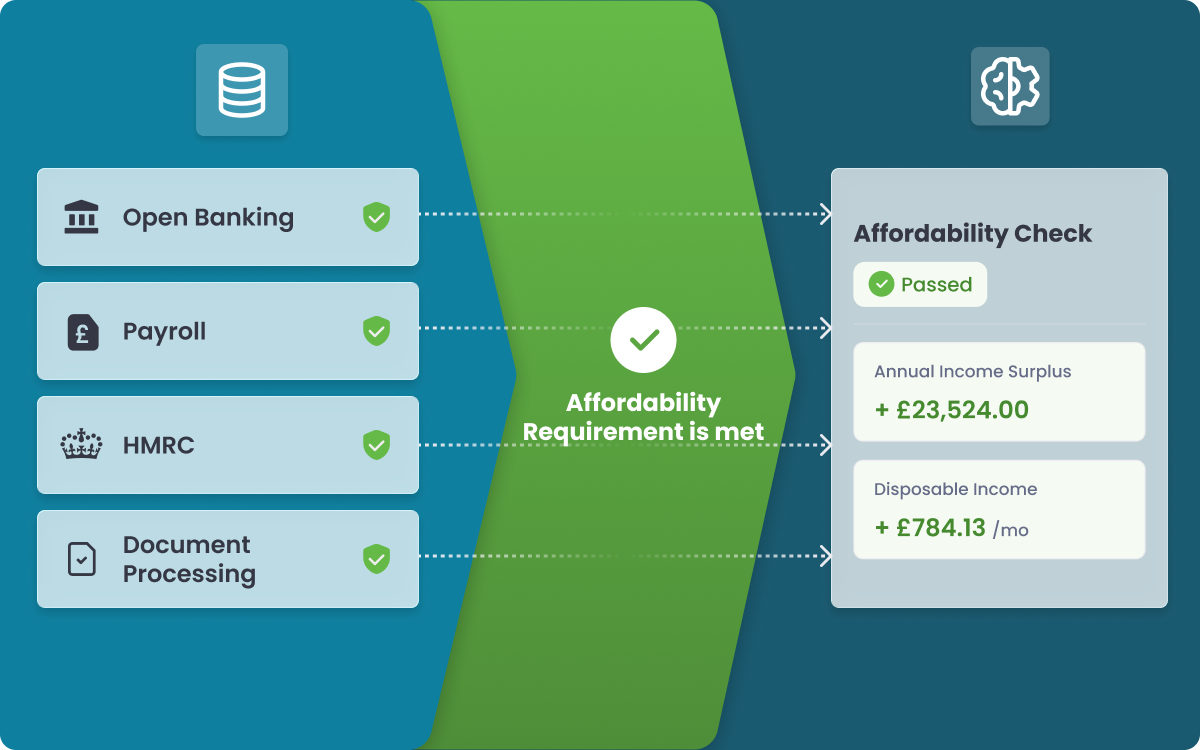

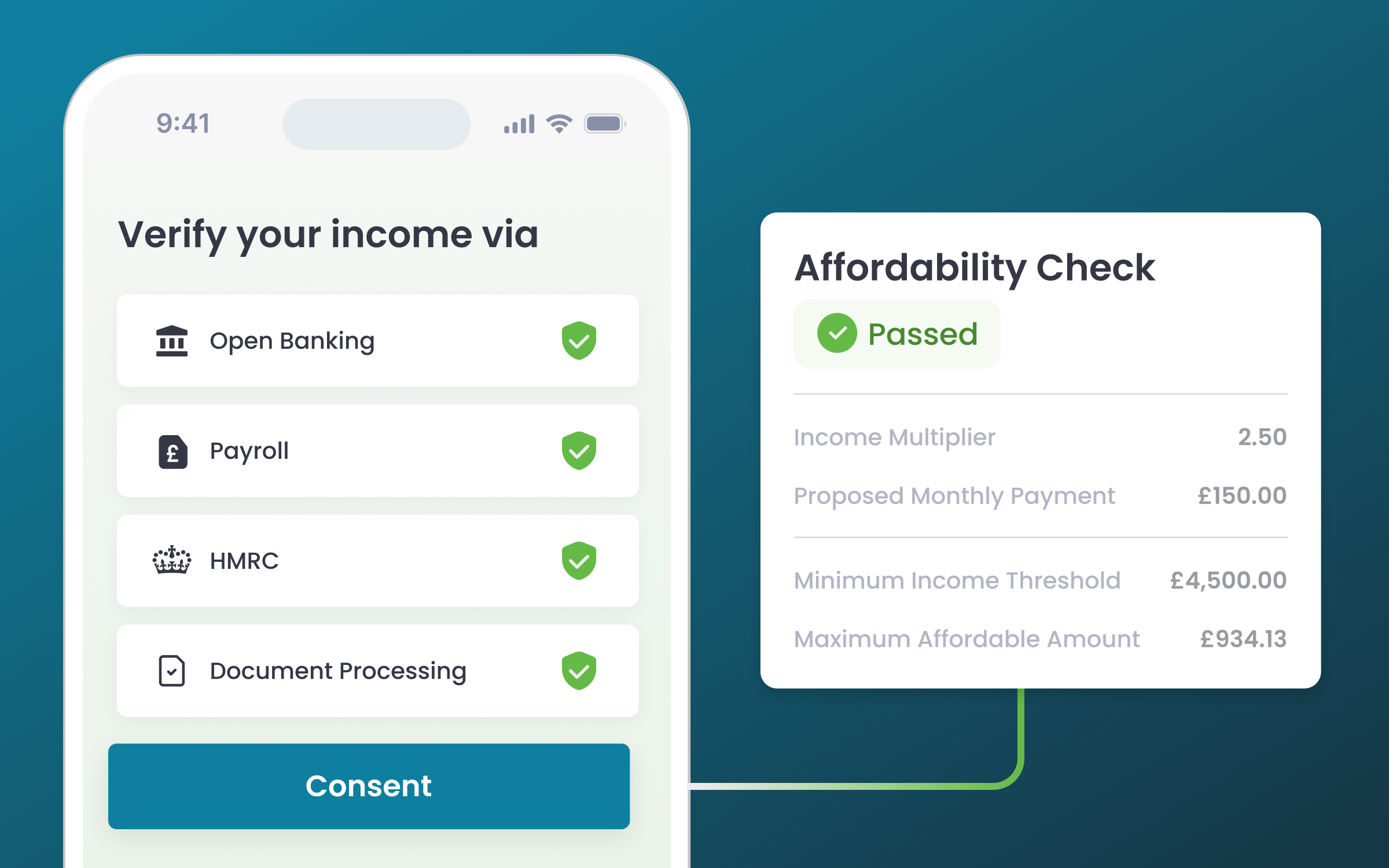

Experian Verify takes a different approach to remove these hurdles. Built on Konfir’s Affordability Waterfall capability, Verify structures a configurable journey around confirming income in line with the lender’s requirements. It brings multiple sources into a permission-based flow and standardises the data into a single API structure, giving lenders a clearer and more connected verification process.

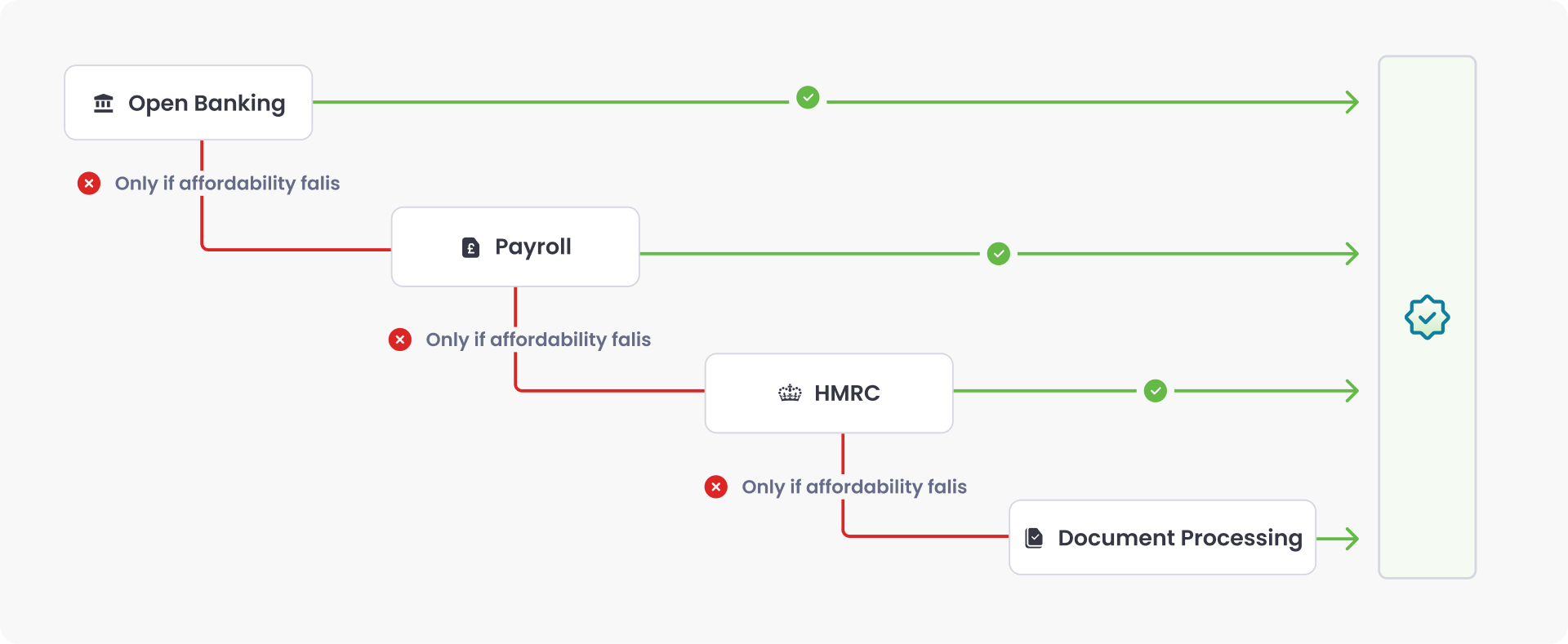

The process begins with Open Banking. If the available income signals are enough to meet the lender’s configured requirements, the Verify journey can stop there and the applicant can continue through the process. If not, the journey can continue through payroll, then HMRC, and then supporting documents where needed. Rather than sending applicants through disconnected fallback workflows, Verify keeps income confirmation in one structured journey and stops once the lender has the evidence it needs. The diagram on page 3 of the amended PDF shows this staged flow clearly, with each source only used if needed.

For unsecured lenders, this means comprehensive income verification becomes a single structured journey instead of a patchwork of disconnected checks. Applicants stay in one flow, and operations teams do not need to interpret partial results across multiple tools before deciding whether enough evidence has been gathered.

It also means verified income can feed cleanly into automated affordability calculations. Experian Verify is not intended to replace a lender’s existing affordability models, policies, or decisioning processes. Instead, it strengthens the verification layer underneath them, so affordability tools have clearer, more consistent, multi-source income evidence to work from.

That’s the value of Experian Verify for unsecured lending: one journey, a clearer way to confirm income, and a stronger path from verified evidence to affordability decision.

.png)

.png)