We use necessary cookies to make our site work. We'd also like to set analytics cookies that help us make improvements by measuring how you use the site. These will be set only if you accept. For more detailed information about the cookies we use, see our Privacy Notice for more information.

From income verification point solutions to affordability verification

Most affordability programmes are a patchwork of vendors and fallbacks. This piece explains the shift to one affordability verification journey, where sources are sequenced until the threshold is met.

WRITTEN BY

Tom McAuliffe

PUblished ON

May 7, 2026

Affordability checks are often described as a data problem. Organisations need to confirm an applicant’s income and compare it against a required threshold, which means obtaining reliable information about employment and earnings. In practice, however, the difficulty rarely lies in defining the affordability rule itself. The complexity usually arises from the way income data is collected and interpreted.

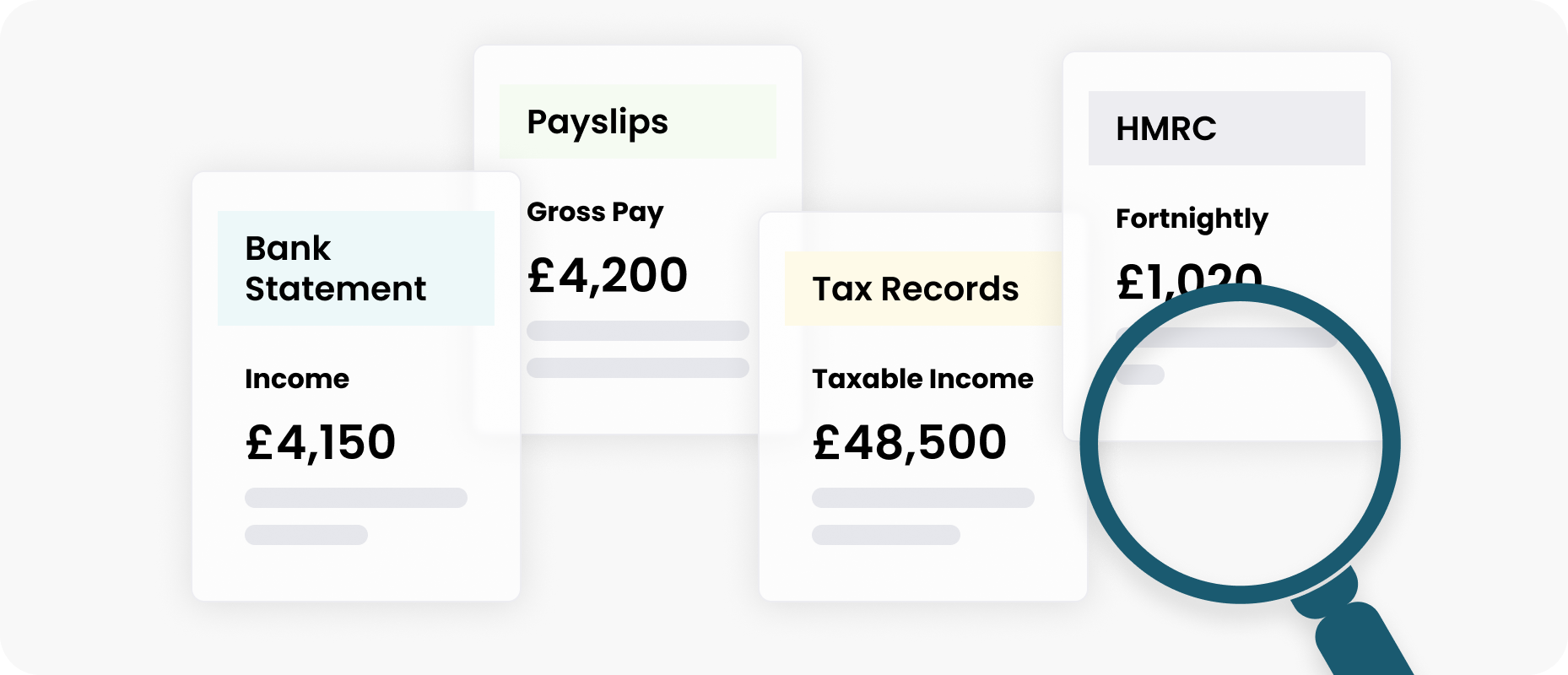

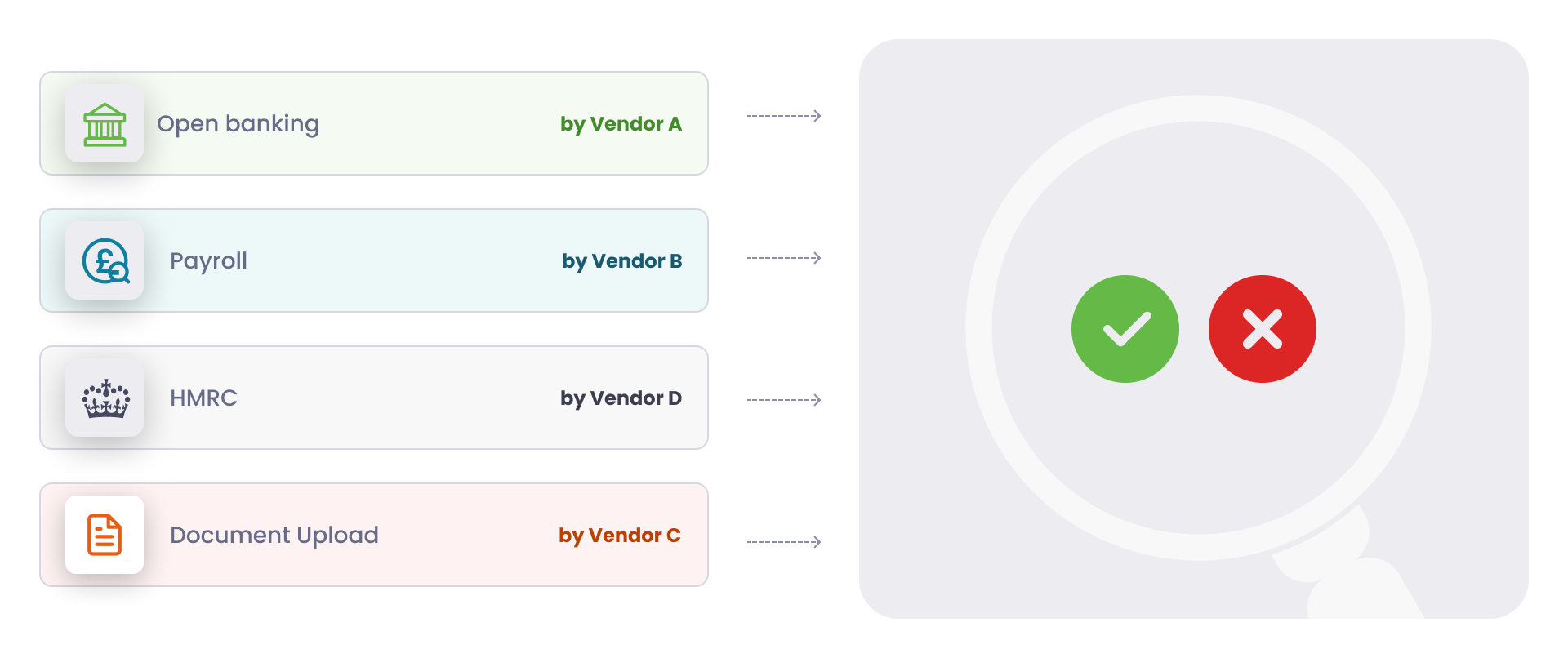

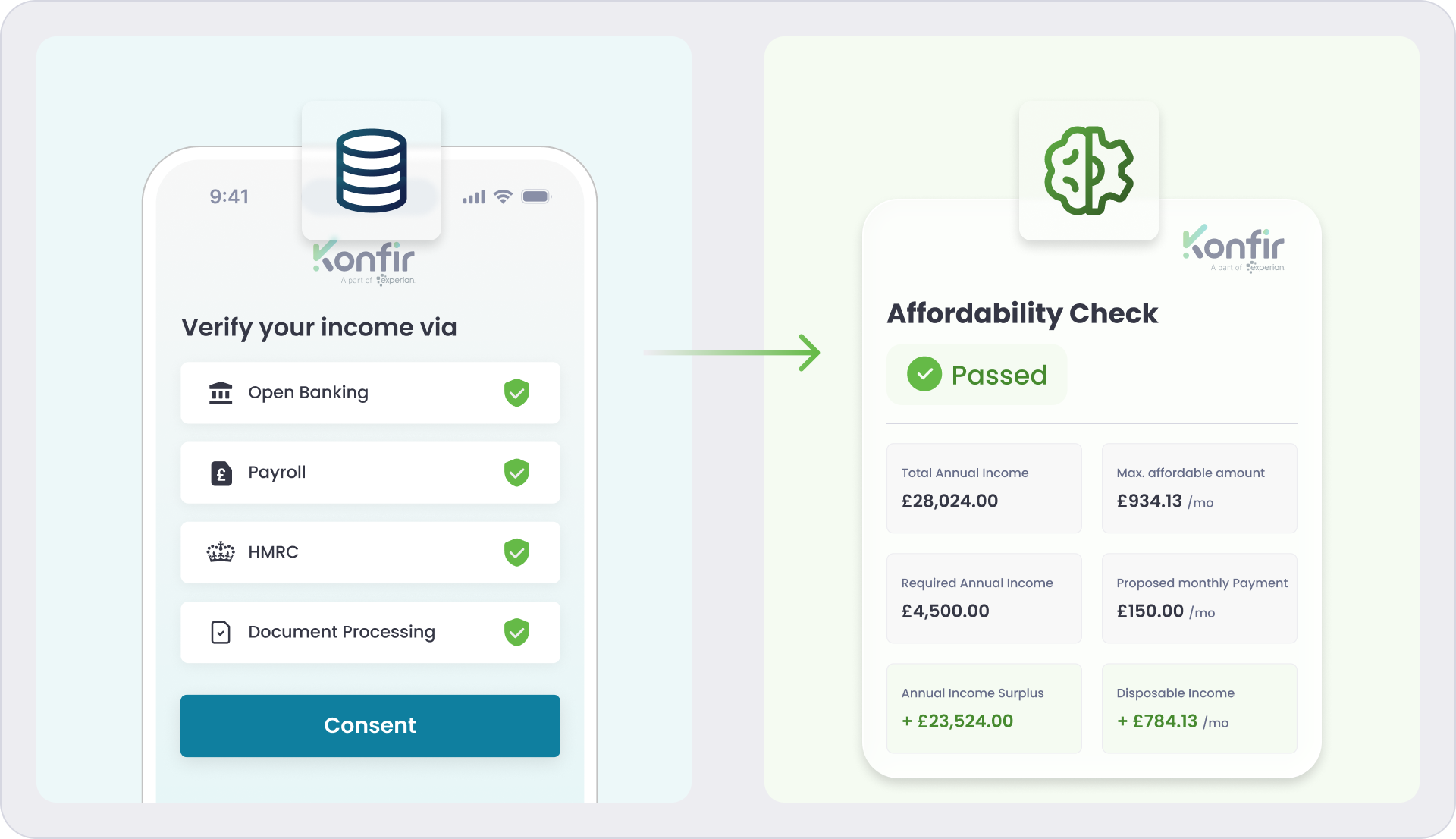

Many organisations have built affordability programmes around multiple verification tools that each provide access to different types of income data. Open Banking provides direct access to income signals from transaction data, payroll data provides structured employer-linked income information, and HMRC records provide verified tax-based income data. Where connected sources alone are not enough to verify all of an applicant’s declared activities, Konfir’s Document Processing completes the journey by converting supporting evidence into structured, fraud-checked results. Each of these methods can provide useful information, but when they are delivered through separate providers they often operate as separate verification processes.

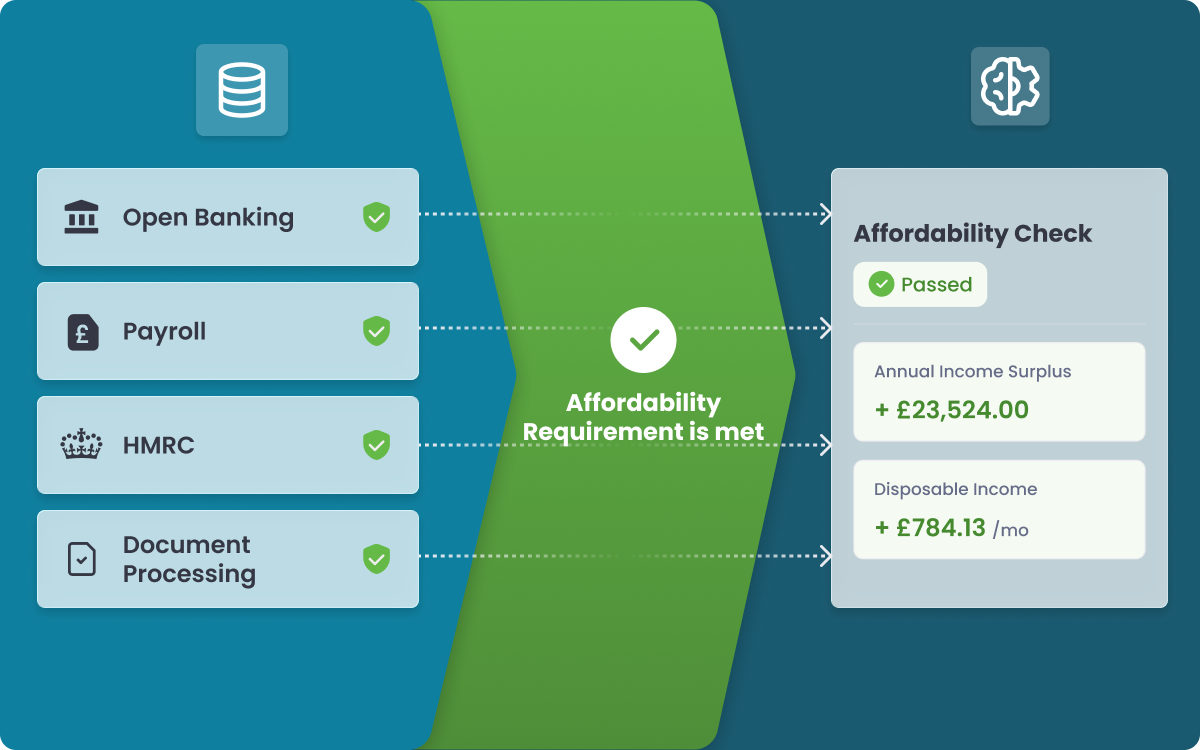

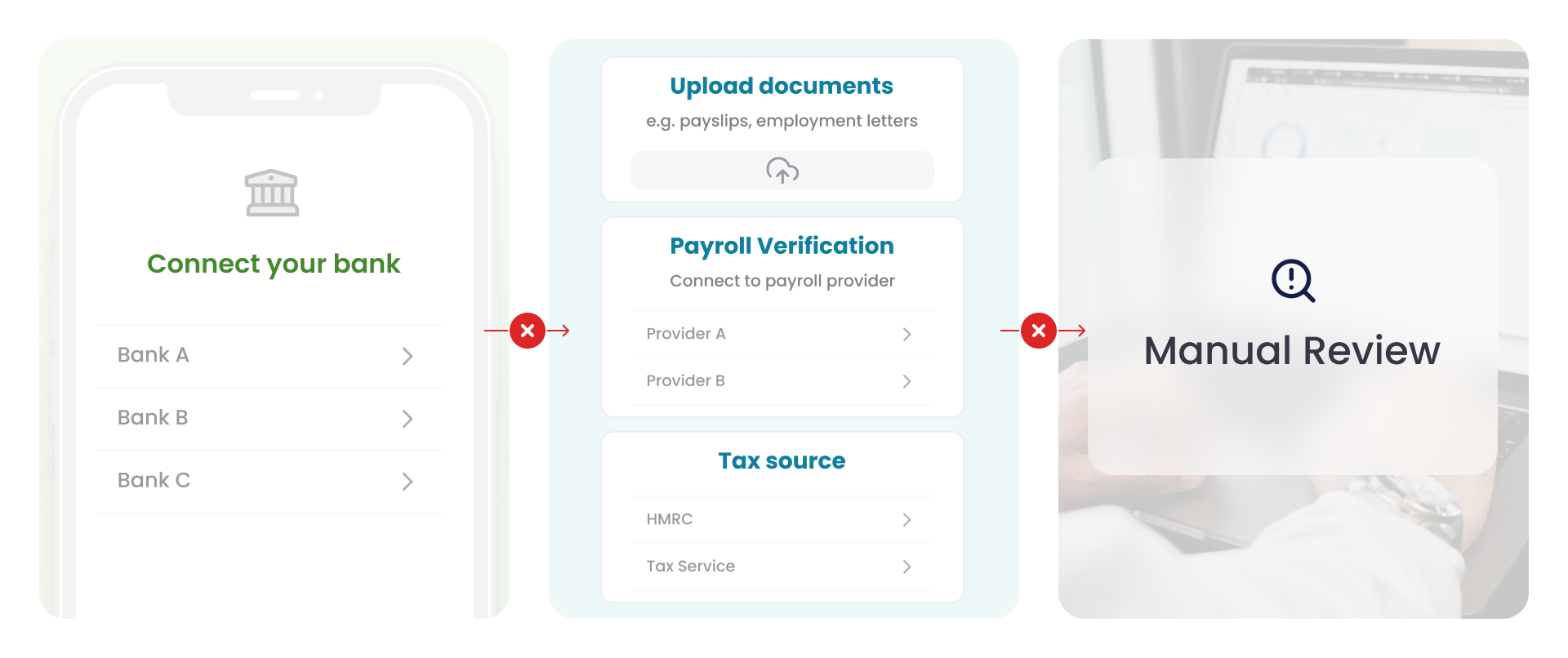

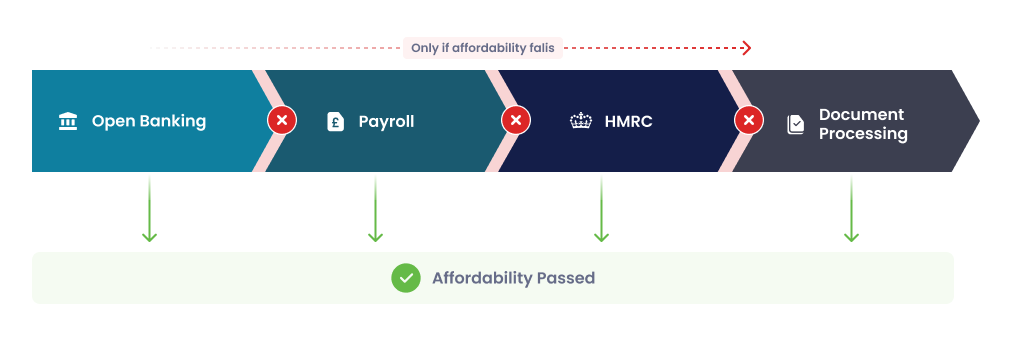

As a result, organisations often end up managing several different workflows within the same affordability journey. An applicant might begin by connecting a bank account through Open Banking. If that does not provide sufficient information, the journey may continue through Payroll, HMRC, or Document Processing within the same structured flow. This is where Konfir changes the model: instead of forcing applicants through disconnected fallback workflows, Konfir sequences income sources in one linear journey, and stops as soon as the affordability requirement is met. Operations teams can then receive a clearer, more consistent result without having to manually stitch signals together before confirming whether the affordability requirement has been met.

Over time, this approach creates an architecture that resembles a stack of income verification tools rather than a single verification process. Each vendor focuses on retrieving data from a particular source, and the responsibility for combining those signals into an affordability outcome sits with the organisation implementing the check.

The introduction of Open Banking for income verification and the Affordability Waterfall changes how this process can be structured.

Open Banking provides a new source of income signals that can be accessed directly within the application journey. In many cases, this allows organisations to identify income quickly and confirm affordability without requesting additional information from the applicant. However, as discussed earlier in this series, Open Banking cannot reliably confirm affordability in every case. Some applicants will still require verification through other sources.

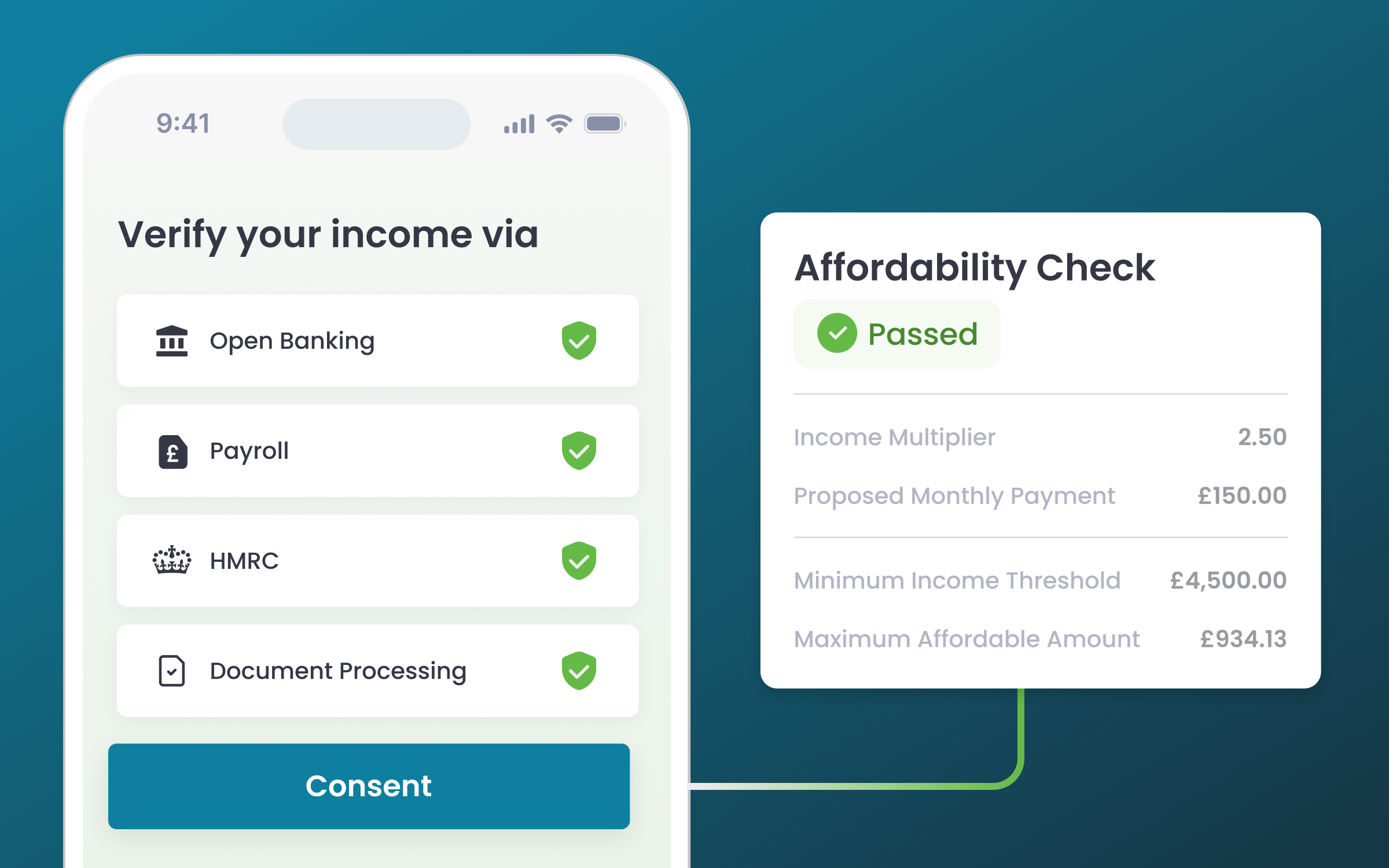

The Affordability Waterfall addresses this by evaluating income sources in sequence against the affordability requirement. Instead of asking whether a particular source can return data, the verification process evaluates whether the verified income from each source meets the required threshold. The journey stops as soon as the requirement is satisfied, which removes the need for separate fallback workflows.

When these two capabilities are combined, affordability verification becomes a single structured process rather than a set of disconnected checks. Applicants move through a single journey that evaluates available income sources in sequence, and organisations receive a clear affordability result based on the threshold they defined.

This model also simplifies how income verification systems are integrated. Because income from Open Banking, payroll data, HMRC records, and documents is returned using the same data model, organisations can integrate the verification process once and use it across multiple income sources without building separate logic for each method.

For organisations that currently rely on multiple income verification providers, this represents a shift in how affordability verification can be implemented. Instead of orchestrating several independent tools and interpreting the results manually, the verification process can be structured around confirming the affordability outcome directly.

.png)

.png)