We use necessary cookies to make our site work. We'd also like to set analytics cookies that help us make improvements by measuring how you use the site. These will be set only if you accept. For more detailed information about the cookies we use, see our Privacy Notice for more information.

Using Open Banking for income verification with Konfir

Open Banking can verify income in seconds, but it is not enough on its own. See how Konfir classifies and standardises income signals, and why multi-source orchestration matters for affordability now.

WRITTEN BY

Tom McAuliffe

PUblished ON

April 2, 2026

Open Banking has become a common way for organisations to access financial data as part of application and verification processes. By allowing applicants to securely connect their bank accounts, it enables organisations to retrieve transaction histories within seconds and analyse the financial activity associated with those accounts.

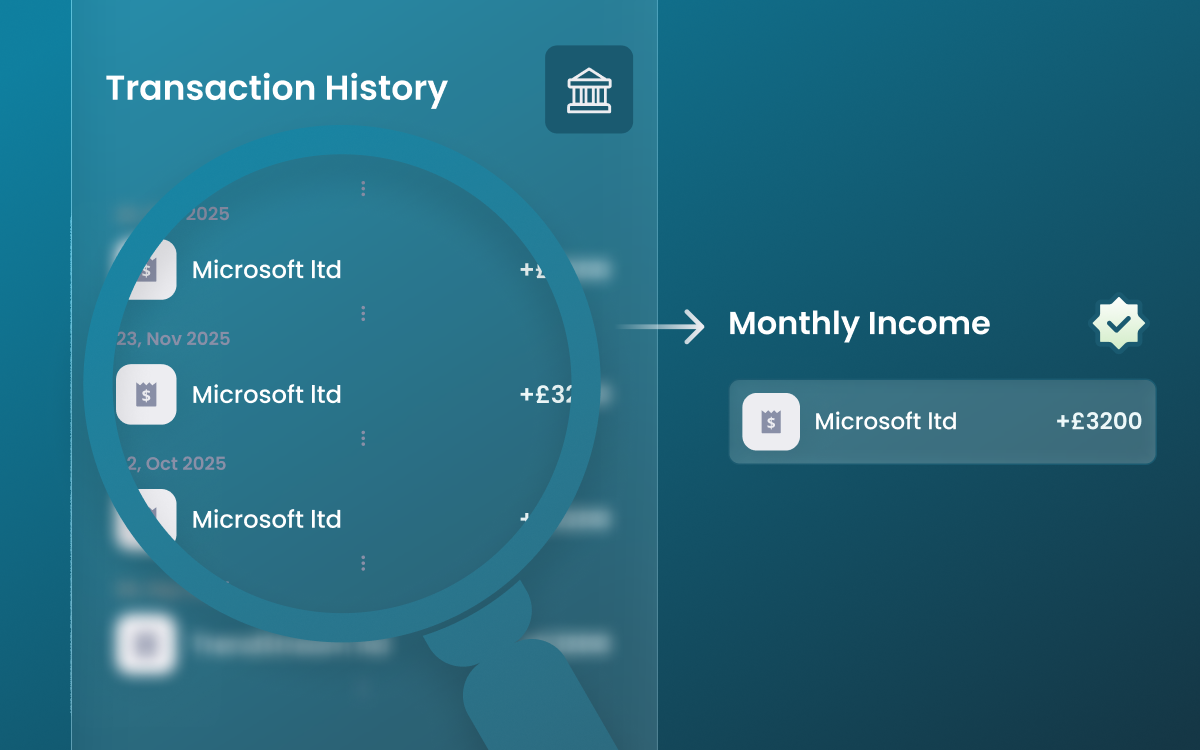

Transaction histories can contain identifiable signals of income. Regular salary deposits from employers often appear as recurring payments, sometimes with recognisable descriptors, and when these patterns are consistent, they can provide a strong indication of employment income. When these signals can be reliably identified, Open Banking data can be used to estimate an applicant’s earnings and support affordability assessments without requiring additional documentation or third-party verification.

This makes Open Banking a useful starting point when organisations need to verify income quickly within an application journey. If the data clearly shows consistent salary payments, income can often be identified and analysed within seconds.

However, the presence of transaction data does not always mean that affordability can be assessed. Data availability itself is not guaranteed, and even when an applicant successfully connects their account, the transaction data returned may not always be sufficient to support an affordability assessment. Open Banking connection rates typically range between approximately 40 and 90 percent. Of those successful connections, only around 60 percent contain transaction histories that provide enough information to assess affordability with confidence.

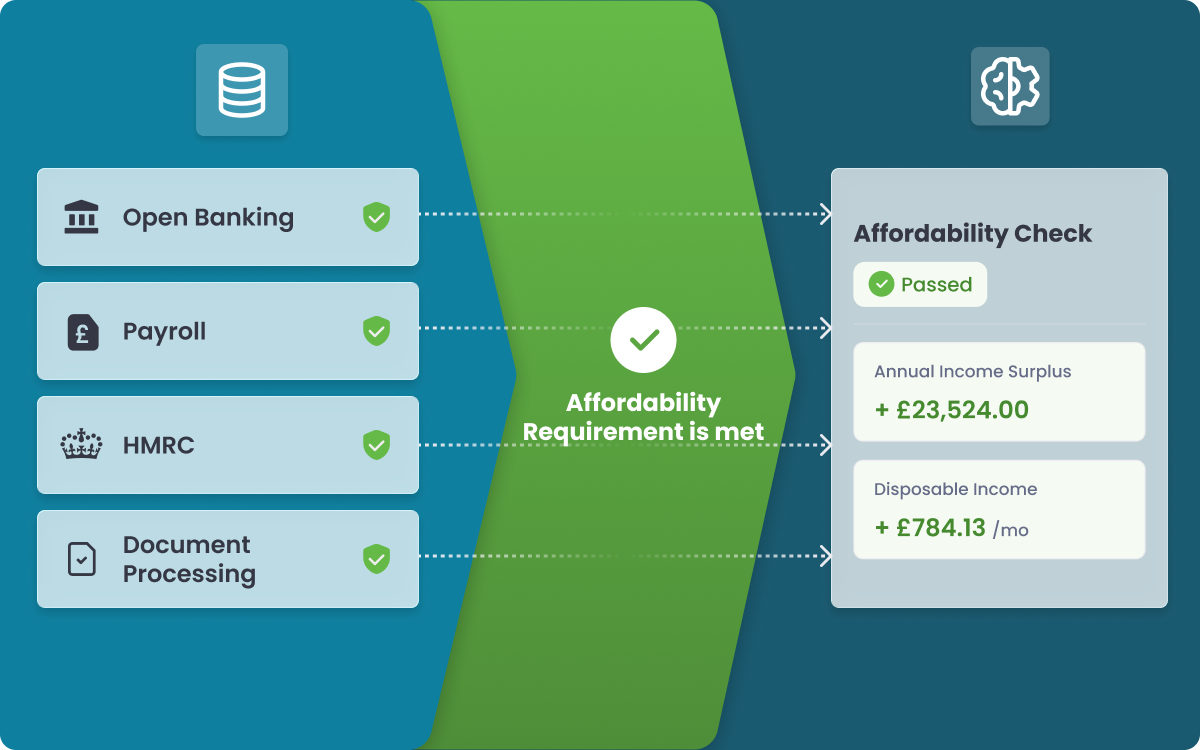

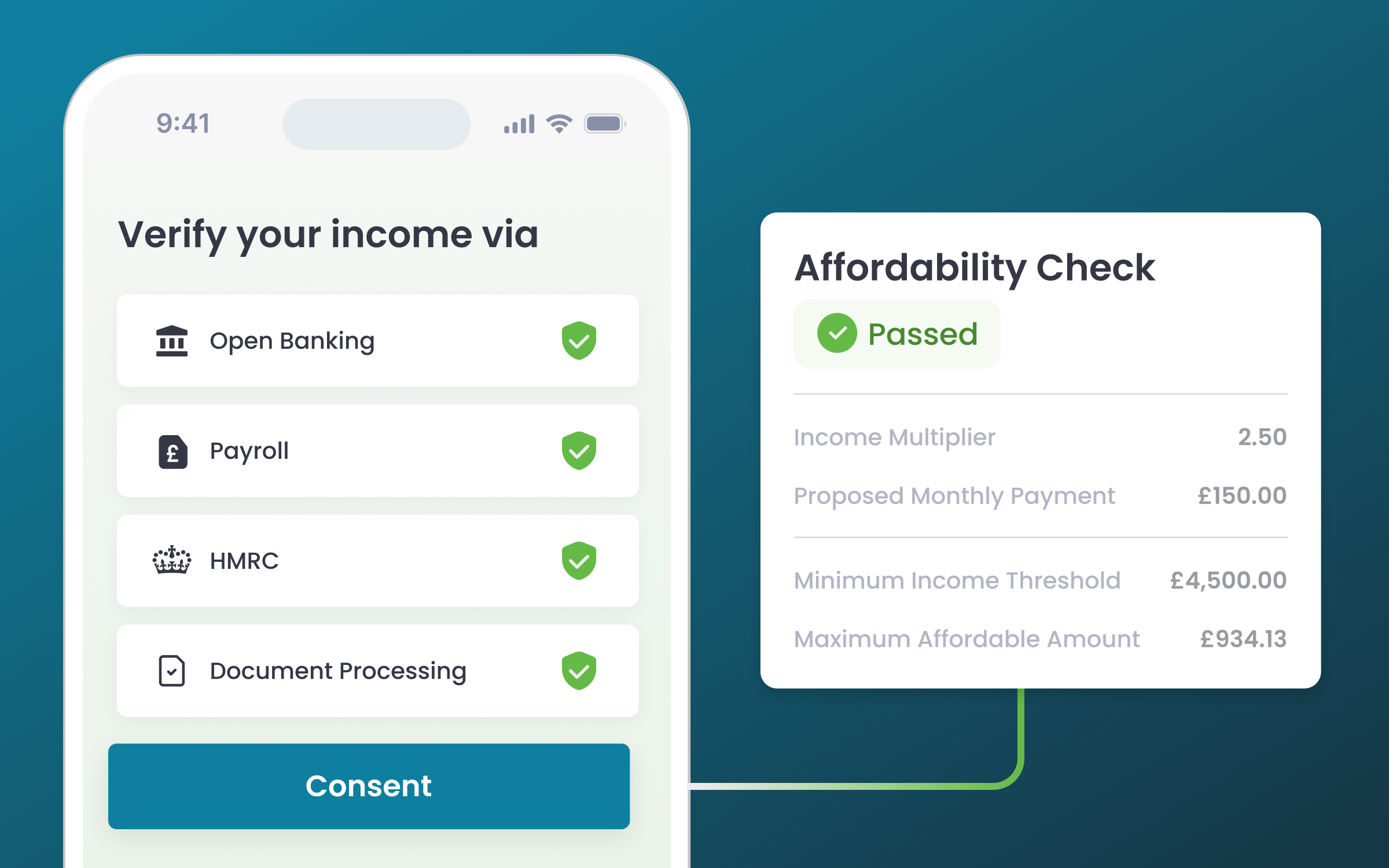

For Open Banking to be useful within income verification, the way transaction data is analysed is critical. Konfir is the only provider currently using a proprietary income classification and categorisation model to transform raw bank transaction data into a structured, verification-ready income signal. Salary payments are identified, standardised, and then matched against Konfir’s employer database so the employer linked to a payment can also be identified. The result is a much stronger signal than transaction analysis alone: Open Banking data becomes usable for employment and income verification, while the underlying transaction data remains available when further context is required.

Another consideration is how the resulting data is returned to clients. One challenge with using multiple income sources is that each source often produces data in different formats, requiring organisations to build separate integration logic for each verification method. Within Konfir, Open Banking data is returned using the same standardised data model as other income sources, such as payroll and HMRC records. This means that regardless of how income is verified, the structure of the response remains consistent and can be interpreted in the same way by downstream systems. Of course, the ability to access more granular data unique to Open Banking is also available through Konfir.

Even with these benefits when using via Konfir, Open Banking should still be viewed as one input into the overall verification process rather than the sole method of confirming affordability. While it can provide valuable signals in many cases, a single data source cannot reliably confirm affordability for every applicant. When Open Banking data is incomplete or insufficient, organisations still need to rely on additional sources such as payroll records, tax data, or supporting documentation.

This is where affordability workflows often begin to fragment. When each verification source is handled separately, applicants may be asked to complete multiple steps and operations teams may need to review data or request documents before a final decision can be made.

.png)